You’ve found the perfect RV. The interior layout is exactly what you dreamed about. The price tag, though? That’s reality-checking you hard. I get it—RVs aren’t cheap. Whether you’re eyeing a $15,000 travel trailer or a $300,000 Class A motorhome, most of us can’t just hand over a check. That’s where RV financing comes in, and honestly, there’s so much more to it than walking into a dealership and saying yes to the first offer.

I’ve spent years researching this stuff for RV buyers, and the difference between a smart loan and a terrible one? It’s tens of thousands of dollars. Your monthly payment, how much you’ll pay in total interest, even whether you get approved at all—it all hinges on understanding your RV loan options before you walk into that dealership or fire up that online application.

This guide walks you through every RV financing option available in 2026, from traditional bank loans to credit union deals to personal loan hacks. You’ll see real numbers, learn exactly what lenders want from you, and walk away knowing exactly which path gets you on the road without destroying your finances.

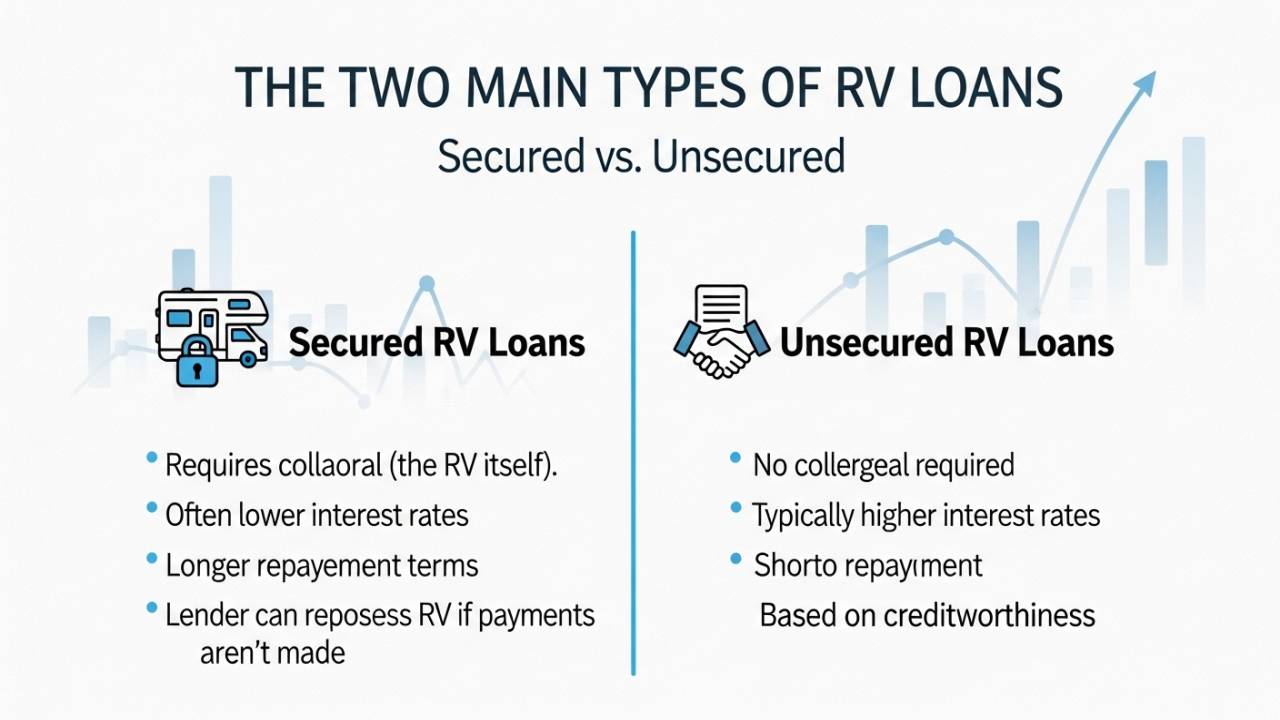

The Two Main Types of RV Loans: Secured vs. Unsecured

Before you compare rates, you need to understand the fundamental difference between how lenders will view your loan.

Secured RV Loans

A secured RV loan uses the RV itself as collateral. If you stop paying, the lender can repossess the vehicle. Sounds harsh, but here’s what you get in return: lower interest rates.

Why? Because the lender’s risk is lower. They have a physical asset to sell if things go south. That translates directly to your wallet—you’ll see interest rates typically 2–6 percentage points lower than unsecured loans.

Most RV financing from banks, credit unions, and specialized RV lenders falls into this category. The trade-off is clear: better rates, but the RV is collateral.

Also Read:- How to Buy a Used RV: Complete Inspection Checklist for First-Time Buyers

Unsecured Personal Loans

An unsecured RV loan (which is really just a personal loan used to buy an RV) doesn’t require collateral. The lender is relying entirely on your credit score and payment history.

That risk means higher rates. Current unsecured RV loan rates can range from just under 7% up to almost 36%, depending on your credit. A personal loan with average rates around 12% will still work for some buyers, especially if you have decent credit, but it’s worth comparing against a secured loan first.

Personal loans also max out around $100,000, so if you’re financing a premium RV, a secured loan is your only option.

RV Loan Options: Where to Get the Money

1. Banks

Traditional banks like Bank of the West and major national banks offer RV financing, and they’re often competitive on rates if your credit score is solid. You’ll need to meet their approval criteria—typically a credit score of 670 or higher—and the application process is similar to an auto loan.

Pros: Lower rates for good credit, fixed payment terms, nationwide availability.

Cons: Stricter credit requirements, longer approval times, less flexibility on terms.

2. Credit Unions

This is where I usually see the best deals for buyers with a membership. Credit unions are member-owned financial institutions that often offer lower interest rates and more personalized service than traditional banks. Navy Federal, for example, offers active and retired military members special discounts on RV loans.

Pros: Lower rates than banks, more personalized service, flexible terms.

Cons: You must be a member (though some are open to anyone), smaller lender network.

3. Dealer Financing

When you walk into an RV dealership, they’ll often pitch their own financing through a network of lenders they partner with. Camping World accesses a network of over 300 trusted lenders to match buyers with the best financing options available.

Pros: One-stop shopping, pre-approval before you pick an RV, dealer handles paperwork.

Cons: Rates may be higher than shopping independently, you might feel pressure to buy.

My advice: Get pre-qualified through dealer financing, but also pre-qualify with a bank or credit union independently. Then compare. You’ll know your best rate walking in.

Also Read:- Norcold RV Refrigerator Not Cooling on Electric or Gas: Fix It in 30 Minutes

4. Specialized RV Lenders

Good Sam Finance Center, FastRVFinancing.com, and LightStream specialize in RV loans. They understand the RV market better than generalist banks—which RV types hold value, which models have resale issues, etc.

Winnebago Financial Services is affiliated with one of the most recognizable names in the RV industry, providing tailored financing solutions for customers of Winnebago vehicles.

Pros: RV expertise, flexible credit requirements (some approve credit scores as low as 600), fast online applications.

Cons: May be pricier than banks or credit unions, limited lender network.

5. Home Equity Loans or HELOCs

If you own a home with equity, you can borrow against it to buy an RV. Home equity loans allow homeowners to borrow against the equity in their home, often at lower interest rates than personal or RV loans, since these loans are secured by your home.

Pros: Lowest interest rates possible, potentially deductible interest.

Cons: Your home is collateral, slower approval, may have closing costs.

Understanding RV Loan Terms: How Long Can You Finance?

One of the biggest levers on your monthly payment is the loan term—how many months (or years) you’ll be paying.

Loan terms for RVs range from 2 to 20 years, depending on the lender, your credit, and the vehicle’s age and price. Here’s the reality:

- Shorter terms (2–5 years): Higher monthly payments, but way less interest paid overall. If you can afford it, this saves thousands.

- Medium terms (7–10 years): Sweet spot for most buyers. Monthly payment is manageable, interest is reasonable.

- Longer terms (15–20 years): Lowest monthly payment, but you’re paying significant interest over time.

Longer RV loan terms can stretch up to 20 years, meaning lower monthly payments. This flexibility is one reason RV loans are attractive—you won’t find a 20-year personal loan for a car, but RV lenders offer it because RVs hold value differently.

The math matters. A $100,000 loan at 7% APR over 10 years costs you about $41,000 in interest. The same loan over 20 years? About $83,000 in interest. That’s an extra $42,000 out of your pocket just to lower the monthly payment by ~$200.

Also Read:- How to Buy a Used RV: Complete Inspection Checklist for First-Time Buyers

Interest Rates and Credit Score: What You’ll Actually Qualify For

Your RV loan interest rate depends on:

- Credit score (biggest factor)

- Loan amount

- Down payment size

- Loan term

- RV age and type

- Your debt-to-income ratio

Most RV lenders require a credit score of at least 670 to qualify for an RV loan, and a higher score can make a significant difference when securing a lower interest rate.

Real rates as of March 2026? It varies wildly. The average interest rate on a personal loan was 12.26% as of March 11, 2026, but RV-specific secured loans typically run lower—somewhere in the 5–9% range for good credit, maybe 10–15% for fair credit.

Bottom line: A 1% rate difference on a $100,000 loan over 15 years means a difference of about $100/month. Shopping around for rates is worth your time.

Down Payments: How Much Do You Need?

Most lenders typically require a down payment of 10-30% of the RV’s purchase price, though some may offer loans without this requirement.

Here’s the strategic thinking: A larger down payment:

- Lowers your loan amount (less interest overall)

- Improves your approval odds

- Shows lenders you’re serious

- Potentially unlocks better interest rates

Let’s say you’re buying a $100,000 RV:

- 10% down ($10,000): You finance $90,000. Monthly payment at 7% for 15 years ≈ $666/month.

- 20% down ($20,000): You finance $80,000. Monthly payment ≈ $593/month (saves ~$73/month).

- 30% down ($30,000): You finance $70,000. Monthly payment ≈ $519/month (saves another ~$74/month).

That $10,000 more upfront saves you ~$1,300 over the loan term. A larger down payment lowers your principal balance and reduces the interest accrued, meaning you’ll pay less over the life of the loan.

Some newer lenders offer zero-down options, but you’ll pay for that flexibility in interest rates and potentially fees.

RV Loan Requirements Checklist

Before you apply, know what lenders will ask for.

| Requirement | What Lenders Look For | How to Prepare |

|---|---|---|

| Credit Score | Minimum 650–670 | Check your credit report at AnnualCreditReport.com; pay off debts before applying |

| Debt-to-Income Ratio | Typically under 50% | Calculate: total monthly debts ÷ gross monthly income; pay down debts if needed |

| Income Verification | Pay stubs, tax returns, W2s | Have 2 months of recent pay stubs ready |

| Employment History | Stable job for 2+ years | Explain job changes if they happened recently |

| Down Payment | 10–30% saved | Have liquid funds ready (bank statements) |

| RV Details | Year, make, model, price | Know the VIN and condition |

| Collateral Value | RV appraisal or market value | Lenders use industry guides (NADA, Black Book) |

Step-by-Step: How to Get an RV Loan Approved

1. Check Your Credit

Don’t apply without knowing your score. Get a free report from AnnualCreditReport.com. If it’s under 650, spend a few months paying down debt and improving your score first. Even a small reduction in your interest rate can save you thousands of dollars over the life of the loan.

2. Estimate Your Budget

How much RV can you actually afford? Use a simple formula:

- Target monthly payment: What’s comfortable? ($500, $700, $1,000?)

- Work backward: Loan calculator → loan amount → RV price – down payment

Don’t get emotionally attached to an RV until you’ve run the numbers.

Also Read:- 10 Best Budget RVs Under $50K for Beginners (2026 Guide + Buying Tips)

3. Get Pre-Qualified with Multiple Lenders

Prequalifying with multiple lenders is a smart first step in the RV loan process, allowing you to explore your financing options without impacting your credit score. Pre-qualification is a soft inquiry—it won’t ding your credit. Get offers from:

- A bank

- A credit union (if you’re a member)

- An RV-specific lender (Good Sam, LightStream, etc.)

- Dealer financing

Compare rates and terms. You’ll now know your best offer before shopping.

4. Shop for Your RV

Now you know your budget and what you qualify for. Find an RV within that range. Don’t stretch.

5. Finalize Your Loan Application

Once you’ve found “the one,” submit your full application. Lenders will:

- Order an appraisal on the RV

- Verify your income and employment

- Check your debt-to-income ratio

- Confirm the RV’s condition and value

6. Review and Sign

Lender sends loan documents. Review all terms carefully—APR, monthly payment, term, fees. Ask about anything unclear. Sign and you’re done.

7. Fund and Take Possession

Lender sends money to the dealership or seller. You take the RV. Hit the road.

Comparing RV Loan Types: Which Is Best for You?

| Category | Details |

|---|---|

| Good credit, new RVs | Interest: 6–9% • Approval: High • Pros: Lowest rates, long terms • Cons: Strict requirements, slower approval |

| Members with good credit | Interest: 5–8% • Approval: High • Pros: Excellent rates, personalized • Cons: Must be member, limited lenders |

| Buyers wanting simplicity | Interest: 7–12% • Approval: Medium • Pros: One-stop shop, pre-approved • Cons: Rates may be higher, pressure to buy |

| Fair/poor credit, unique RVs | Interest: 7–15% • Approval: Medium–High • Pros: RV expertise, flexible credit • Cons: Potentially higher rates |

| Lower-priced RVs, bad credit | Interest: 12–36% • Approval: Medium • Pros: Quick funding, no collateral • Cons: High rates, lower max loan amounts |

| Homeowners, large loans | Interest: 5–8% • Approval: High • Pros: Lowest rates, large amounts • Cons: Home is collateral, closing costs |

Also Read:- RV Refrigerator Not Cooling? Troubleshooting & Solar Power Fix

Red Flags and Mistakes to Avoid

Don’t rush. Pre-qualify with at least three lenders. A 1% rate difference costs you thousands.

Don’t ignore the APR. Advertised rates sound great (“4.99% APR!”), but real-world rates are higher. Ask for your actual APR, not just the interest rate.

Don’t max out your budget. Just because you qualify for a $150,000 loan doesn’t mean you should borrow it. Can you afford the payment, insurance, maintenance, fuel, and campground fees all together?

Don’t skip the appraisal. A low appraisal can tank your loan or force you to put down more money. Get an independent appraisal if the lender’s valuation seems off.

Don’t finance add-ons. Extended warranties, gap insurance, paint protection? These sound safe but add $5,000+ to your loan. Only finance them if you truly need gap insurance (and you might, depending on the RV).

Don’t assume dealer financing is cheapest. It’s convenient, but you’ll almost always get better rates shopping independently.

Frequently Asked Questions

What’s the longest RV loan term available?

20 years. This is most common for new, high-end motorhomes. Used RVs typically max out at 10–15 years, and older RVs (10+ years old) may only qualify for 5–7-year terms.

Can I get an RV loan with bad credit (600 or lower)?

Tough, but not impossible. Specialized lenders like Good Sam will consider credit scores as low as 600, but you’ll pay 15–25% APR and need a larger down payment (25–30%). Consider waiting a few months to improve your score—it’ll save you thousands.

What if I’m buying a used RV from a private seller, not a dealer?

You can still get a loan. Most lenders finance private-party purchases. You’ll need a pre-purchase inspection and the seller’s title. Timeline is longer because the lender will appraise the vehicle.

Can I refinance my RV loan later?

Absolutely. If interest rates drop or your credit improves, refinancing can lower your rate and save thousands in interest. Check rates annually.

Is gap insurance worth it on an RV loan?

Gap insurance covers the difference between what you owe and the RV’s actual cash value if it’s totaled. RVs depreciate fast in year one, so if you’re financing 90%+ of the value, gap insurance is smart. If you’re putting 30%+ down, skip it.

What if the RV doesn’t pass inspection after I’m approved?

You’re not obligated to buy. But the lender has already done an appraisal and conditional approval on that specific RV. You’ll need to find another RV that appraises similarly, or renegotiate the loan amount.

Can I pay off my RV loan early without penalties?

Most RV loans have no pre-payment penalties. Pay it off whenever you want. That said, run the math—if you’ve only got a year left at 7% APR, the interest savings might not be worth cashing out other investments.

Conclusion:

Your RV financing decision sets the tone for your entire RV ownership experience. A smart loan means affordable monthly payments and years of stress-free adventures. A bad loan? You’re bleeding money on interest while feeling trapped in a commitment you can’t afford.

The good news: You now know exactly what to look for. You understand the difference between secured and unsecured loans, you know where to find the best rates, and you know the exact steps to follow from pre-qualification to signing.

The move? Start pre-qualifying today. Get offers from at least three lenders. Compare not just rates, but terms, fees, and flexibility. Take your time. There’s no rush—the RV isn’t going anywhere, and shaving even 1% off your interest rate could save you $10,000 or more over the life of your loan.

Your perfect RV adventure is out there. Make sure your financing doesn’t get in the way.

Ready to get pre-qualified? Start with your bank or credit union, then compare rates from Good Sam, LightStream, or your local RV dealership. You’ve got this.

Saket Kumar is a veteran RV writer and enthusiast who has financed and owned multiple RVs. This guide is based on current rates and terms as of March 2026. Always verify current interest rates and loan terms directly with lenders before applying.